Know all about Account Aggregator Network- a financial data-sharing system

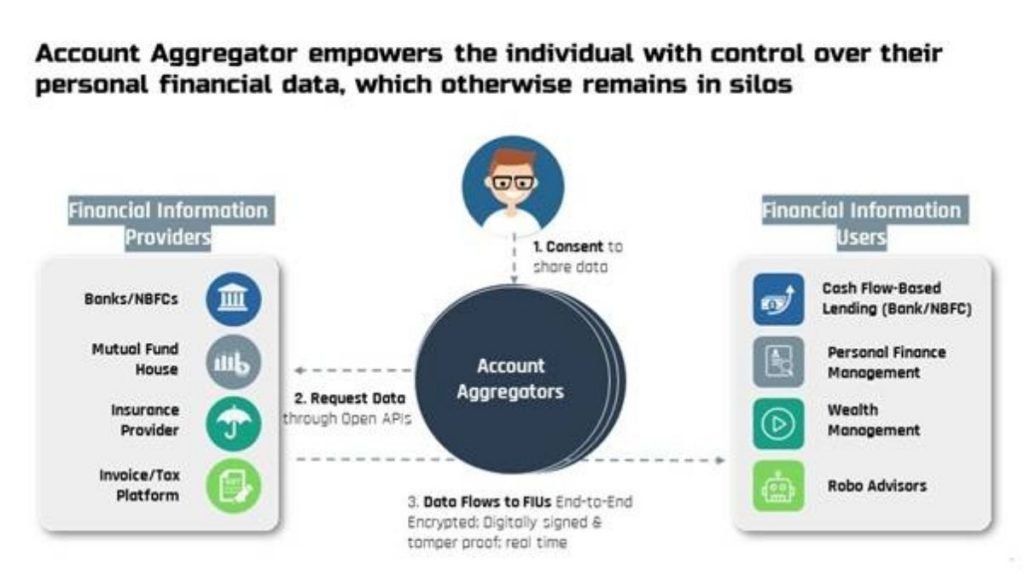

Last week India unveiled the Account Aggregator (AA) network, a financial data-sharing system that could revolutionize investing and credit, giving millions of consumers greater access and control over their financial records and expanding the potential pool of customers for lenders and fintech companies. Account Aggregator empowers the individual with control over their personal financial data, which otherwise remains in silos.

This is the first step towards bringing open banking in India and empowering millions of customers to digitally access and share their financial data across institutions in a secure and efficient manner.

The Account Aggregator system in banking has been started off with eight of India’s largest banks. The Account Aggregator system can make lending and wealth management a lot faster and cheaper.

- What is an Account Aggregator?

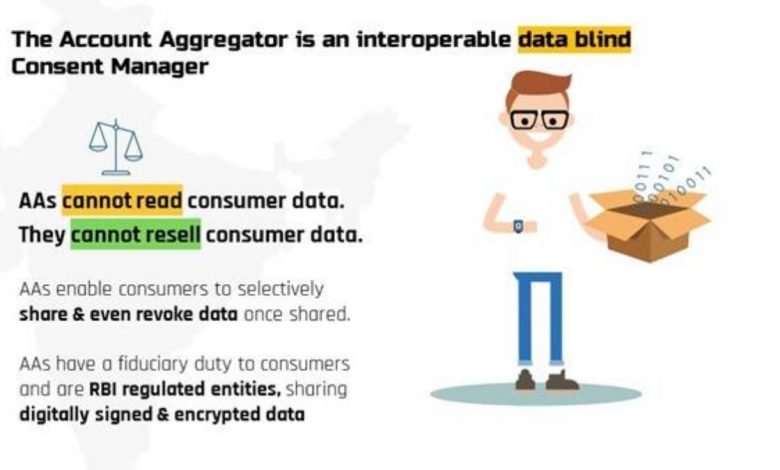

An Account Aggregator (AA) is a type of RBI regulated entity (with an NBFC-AA license) that helps an individual securely and digitally access and share information from one financial institution they have an account with to any other regulated financial institution in the AA network. Data cannot be shared without the consent of the individual.

There will be many Account Aggregators an individual can choose between.

Account Aggregator replaces the long terms and conditions form of ‘blank cheque’ acceptance with granular, step-by-step permission and control for each use of your data.

2)How will the new Account Aggregator network improve an average person’s financial life?

India’s financial system involves many hassles for consumers today — sharing physical signed and scanned copies of bank statements, running around to notarise or stamp documents, or having to share your personal username and password to give your financial history to a third party. The Account Aggregator network would replace all these with a simple, mobile-based, simple, and safe digital data access & sharing process. This will create opportunities for new kinds of services — eg new types of loans.

The individual’s bank just needs to join the Account Aggregator network. Eight banks already have — four are already sharing data based on consent (Axis, ICICI, HDFC, and IndusInd Banks) and four are going to be able to shortly (State Bank of India, Kotak Mahindra Bank, IDFC First Bank, and Federal Bank).

3) How is Account Aggregator different from Aadhaar eKYC data sharing, credit bureau data sharing, and platforms like CKYC?

Aadhaar eKYC and CKYC only allow sharing of four ‘identity’ data fields for KYC purposes (eg name, address, gender, etc). Similarly, credit bureau data only shows loan history and/or a credit score. The Account Aggregator network allows sharing of transaction data or bank statements from savings/deposit/current accounts.

4) What kind of data can be shared?

Today, banking transaction data is available to be shared (for example, bank statements from a current or savings account) across the banks that have gone live on the network.

Gradually the AA framework will make all financial data available for sharing, including tax data, pensions data, securities data (mutual funds and brokerage), and insurance data will be available to consumers. It will also expand beyond the financial sector to allow healthcare and telecom data to be accessible to the individual via AA.

5) Can AAs view or ‘aggregate’ personal data? Is the data sharing secure?

Account Aggregators cannot see the data; they merely take it from one financial institution to another based on an individual’s direction and consent. Contrary to the name, they cannot ‘aggregate’ your data. AAs are not like technology companies that aggregate your data and create detailed profiles of you.

The data AAs share is encrypted by the sender and can be decrypted only by the recipient. The end-to-end encryption and use of technology like the ‘digital signature’ makes the process much more secure than sharing paper documents.

6) Can a consumer decide they don’t want to share data?

Yes. Registering with an AA is fully voluntary for consumers. If the bank the consumer is using has joined the network, a person can choose to register on an AA, choose which accounts they want to link, and share their data from one of their accounts for some specific purpose to a new lender or financial institution at the stage of giving ‘consent’ via one of the Account Aggregators. A customer can reject the consent to share a request at any time. If a consumer has accepted to share data in a recurring manner over a period (eg during a loan period), it can also be revoked at any time later as well by the consumer.

7) If a consumer has shared my data once with an institution, for how long can they use it?

The exact time period for which the recipient institution will have access will be shown to the consumer at the time of consent for data sharing.

8) How can a customer get registered with an AA?

You can register with an AA through their app or website. AA will provide a handle (like username) that can be used during the consent process.

Today, four apps are available for download (Finvu, OneMoney, CAMS Finserv, and NADL) with operational licenses to be AAs. Three more have received in-principle approval from RBI (PhonePe, Yodlee, and Perfios) and may be launching apps soon.

9) Does a customer need to register with every AA?

No, a customer can register with any AA to access data from any bank on the network.

10) Does a customer need to pay the AA for using this facility?

This will depend on the AA. Some AAs may be free because they are charging a service fee to financial institutions. Some may charge a small user fee.

11) What new services can customers access if their bank has joined the AA network of data sharing?

The two key services that will be improved for an individual are access to loans and access to money management. If a customer wants to get a small business or personal loan today, there are many documents that need to be shared with the lender. This is a cumbersome and manual process today, which affects the time taken to procure the loan and access to a loan. Similarly, money management is difficult today because data is stored in many different locations and cannot be brought together easily for analysis.

Through Account Aggregator, a company can access tamper-proof secure data quickly and cheaply and fast-track the loan evaluation process so that a customer can get a loan. Also, a customer may be able to access a loan without physical collateral, by sharing trusted information on a future invoice or cash flow directly from a government system like GST or GeM.

Disclaimer: this is an official press release by pib.